Tony French

Among the profusion of paper crossing my desk this week was a media release from Micah Challenge, Shining the light on Global Tax Dodging. The title caught my eye for a couple of reasons: I’m a Tax Agent with a professional interest, of course, and I wanted to know just what were the ‘dodgy’ tax practices. And also because I had not heard of the Micah Challenge.

It turns out Micah Challenge is a worldwide collection of church groups and individuals who, in their commitment to social justice, advocate particularly for governments to meet the Millennium Development Goals to reduce global poverty.

Good on them, I thought, as I turned back to their media release which had been issued following a meeting with politicians in Canberra to address the issues of taxation of multinational enterprises, and to point out that, as a result of multinational tax dodging, poor countries suffer a disproportionately greater loss of their tax revenues than wealthy countries.

The media release was designed to arouse the reader’s righteous indignation about this massive tax cheating and its consequences. But multinationals, merely by operating across national borders, were by their definition tax cheats and dodgers. What they were doing was not necessarily illegal, my Tax Agent voice said. The media release went on to state that “more money was pulled out by large multinational corporations than was stolen by corrupt politicians and dictators”. That I found a bit hard to believe, even in the unlikely event such figures are actually available. What about the monstrous – and probably far greater – amounts of money laundered globally from criminal and terrorist activities?

My initial sense of righteous indignation was deflating. The expression ‘tax dodging’ is emotive, applying both to tax avoidance (legal) and to tax evasion (illegal). International tax ‘minimisation’ is less a consequence of little or no corporate ethics than of loopholes, lax state administration, and failure of international cooperation. Its legitimate offspring is the ‘tax haven’, albeit its use often illegitimate.

Tax havens are not the creation of dodgy corporations, but in fact State creations. Generally, they are characterised by low or no taxes, low or no regulation, and are – without public registers and high secrecy – hugely helpful. These ingredients frequently coalesce in some idyllic island location with an allure so tempting to all but the most patriotic holding corporation. Think of it as State-sponsored support for maximising your corporate profits by minimising your tax.

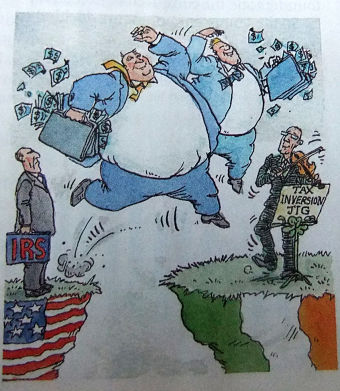

Tax havens are not the monopoly of dodgy governments; many governments actually encourage tax havens, even though their countries have no golden beaches or swaying palm trees. The Irish government succeeded in making Ireland a tax haven, having a deleterious knock-on effect for other European governments which had to match or even better the attractive Irish corporate tax rate of 10%. With consequent lowered tax revenues, these governments had reduced funds for welfare, education, and health. It is little surprise, therefore, that social services and infrastructure were sacrificed. I recall a recent proposal to make Northern Australia a ‘special economic zone’ – aka a tax haven – to ‘encourage’ development.

Most tax havens don’t, however, involve a shift in real economic activity, but a paper shift which encourages tax avoidance; it’s then a competitive corporate race to see who will pay no tax at all. And it’s legal, for although it’s not the best place to do business, it’s the best place in which not to pay tax.

No surprise either that the cumulative global tax take from multinationals has been declining, although their revenues and profits keep rising. And oddities emerge such as the fact that the British Virgin Islands, a tiny Caribbean coral island but large tax haven, is the second biggest investor in China.

Having a tax haven is handy for a multinational, but there is additional corporate welfare, thanks to the marvel of ‘transfer pricing’ whereby entities of the same company can also pay little or no tax. Profits shift to low- or non-taxing countries internally and across borders, and expenses to countries with high levels of taxation. Never underestimate corporate creativity. But credit really has to be given to the nations that allow this creativity to flourish.

Other than being indignant and tut-tutting about all this, what can be done to salvage national tax revenues and clip the wings of the transnational corporation? As it turns out, there is quite a bit that can be done according to the Friedrich Ebert Stiftung, which, like Micah Challenge, fosters debate on global matters, and is also committed to correcting the abuses of international tax rorting.

Some examples: ‘Arms length’ pricing tackles transfer pricing whereby tax authorities can calculate prices, production, and profits by reference to comparable enterprises. Think of the ATO’s industry standard for taxi drivers, pizza proprietors, and others operating in the cash economy. Intangibles such as intellectual rights are difficult to assess on this method – an advantage to Google and Apple. A significant chunk of our Income Tax Act is devoted to regulating transfer pricing.

Banning ‘letterbox’ companies also works. Two hundred thousand companies have their registered offices at a single Delaware USA address, yet only 80 people work in the building, presumably collecting and distributing the mountain of mail.

Successful regulation requires information, so transparency is important. Countries need to provide comparable details, assets, sales, employee numbers, and payments to each government. ‘Country by country’ reporting allows comparisons to be made and mismatches identified. Transparency also dictates details of ‘beneficial ownership’; in other words, who really owns or benefits from the entity? Proper public registers are a prerequisite.

Such international cooperation might just highlight then remove contradictions between countries’ tax systems, whereby, for example, an asset is not taxed in one country but is deductible in another. That’s wonderfully known as ‘double-non taxation.’

Double Taxation Agreements or bilateral tax agreements between countries may address such delightful anomalies, and even adventurously ban corporate entities and individuals going ‘treaty shopping’, searching for the most benign tax jurisdictions.

And a powerful way to minimise tax avoidance is to impose a ‘withholding’ tax, which is simply nothing more than taking tax from the money before it has a chance to depart. Taxing at source captures income and capital revenues.

Another method worth considering is ‘unitary’ taxation. As its name suggests, you tax the parent and all its subsidiaries as one, irrespective of where the subsidiaries are located. Too idealistic, you say. Well, unitary tax applies in California, and now we know why Hollywood (for whom it was intended) has not been accused of interstate or international tax dodging. The EU is currently considering implementing just such a tax.

Finally, States are concerned about their increasing tax leakages, so now taxation of multinational entities is at last on their cooperative agenda. The Group of 20 and the OECD are taking steps, reported The Australian (23.2.14), to end global tax havens and make sure multinational and digital companies pay their fair share of tax. A day or two later, this newspaper reported the Australian Commissioner of Taxation announcing that the concept of the tax haven was dying, and it was only a matter of time before dodgers were caught. The imminent death of the tax haven might be much exaggerated, but the Commissioner did warn all taxpayers with offshore assets to declare their interest ahead of the coming global crackdown.

At the G20 meeting to be held in Australia later in 2014, high on the agenda is putting an end to global tax havens. Micah Challenge is there to remind Australia as host nation to push hard for overdue regulatory reform, which can only be achieved by global consensus arising out of such gatherings.

The G20 comprises the leading economic nations who, by definition, have good systems of administration able to implement measures limiting international tax dodging. But what of poorer countries, many of whom only have partial tax systems and generally poor administration? Many are tax havens by inadvertence rather than by intent.

If the rich nations can at last control the international flight of tax revenues, then they will have increased revenue to fund foreign aid to assist developing nations establish their own responsible revenue-collecting institutions.

The G20 nations first need to put their own tax houses in order and to cooperate. Until then, corporations and individuals will legally and illegally continue to move money (legal and illegal) to hidey-hole tax havens. When you think about it, it’s mostly the G20’s own rich corporations and citizens who are using tax havens in the first place.♦

Tony French is a Melbourne lawyer, and a member of the SPC board of directors.